Economic crises carry with them hugely devastating results: high rates of unemployment and bankruptcy are emblematic of the more modern ones. Often, a crisis is not precipitated by a flaw in the overall economy but instead a dangerous practice in a sector of that economy. Perhaps that sector has companies or individuals who have undertaken a course of action that threatens the market, and perhaps no authority figure—governmental or otherwise—can curb or stop that dangerous behavior and prevent the damage from being done. By 1873, the American railroad industry had become an industry asking for a crisis: throughout the country—and increasingly in Europe—the American railroad companies had been a popular investment; the lure of high returns was too strong for investors to resist, and the tinderbox for the impending blaze would be the bonds of railroad companies. Those bonds were the sought after investment of the time and had been collateralized—just as a piece of real estate is collateralized for a mortgage—several times over (therefore inflating the value of the bonds, the volume of the railroad bond market, and the risk of the investments). Investors, through their greed, were guaranteeing that when the market did face a disruption—and it inevitably would—that disruption, that spark, would be the beginning of a years-long economic depression.

Investing in railroads—and its counterpart industries—was not simply an American trend. In the early 1870s, many British investors began to put their funds not only into the American railroad industry but also pivoted their investments from the Austro-Hungarian grain industry to the American wheat industry.[i] Because of the growing railroad industry, and the lower prices of shipping that it fostered, the American wheat crop had become highly competitive. The Austrian banks, invested in their country’s grain crops and cattle trade, began to fail as a result of being undercut.[ii] As is typical with a crash, because capital would be drying up and the default rate on loans was expected to increase, interest rates began to rise in Europe; and because a global market was blossoming, those rises in interest rates were set to affect loans that German, Dutch, and English investors had in American railroads.[iii] Railroad bonds had become a massive market by this time: while in 1867 the total debt in railroad bonds amounted to $416 million, that debt had ballooned to $2.23 billion by 1874.[iv] The market had inflated far beyond its worth. Because there was the potential for high returns on investment, there was no shortage of investors, but many of those investors became more wary when they learned that the railroads were using the interest in new bonds to pay interest on existing loans; with that knowledge (which indicated that the railroad companies were not the most financially sound companies in which to invest), investors went back to putting funds in European markets.[v] By late 1873, “American railroads lacked the revenue to pay both expenses and interest, and without access to fresh capital, they would fall into” bankruptcy, then receivership.[vi]

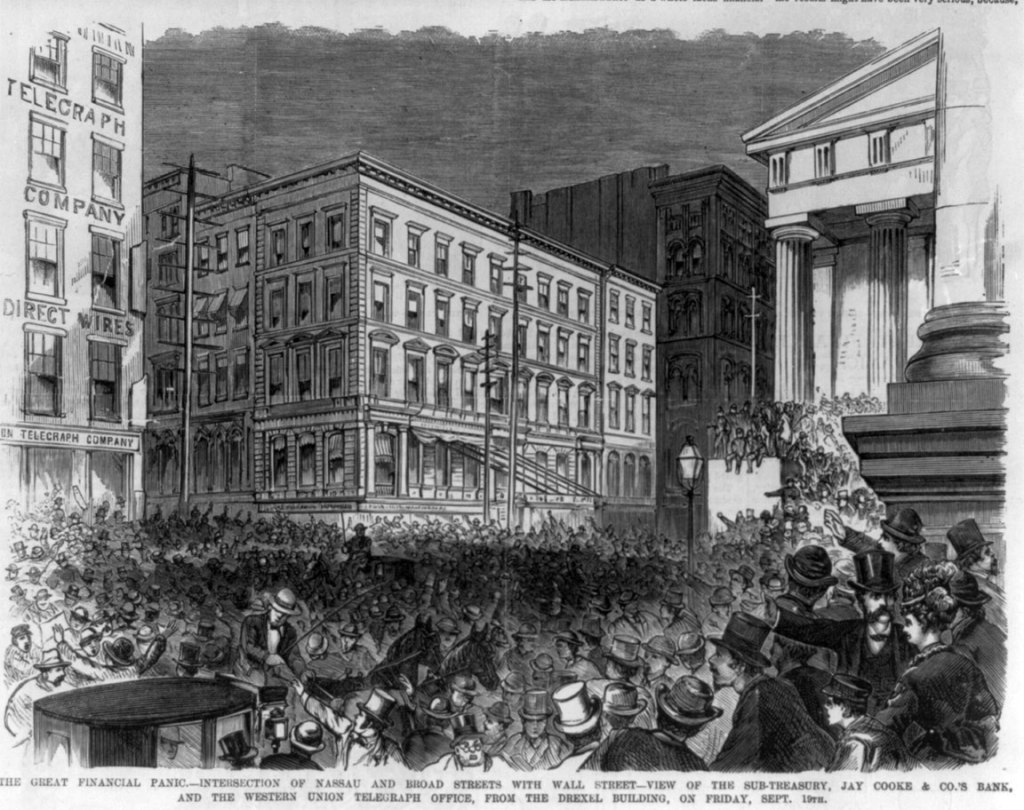

One of the most prominent railroads in America, the Northern Pacific Railroad (which the Jay Cooke & Company operated), began to experience trouble during this time. Jay Cooke initially had success raising funds by bringing in small investors to buy up bonds, but as the crisis was coming to a head, he had sold an extraordinary number of bonds—which were the only security for the company’s loans—and those bonds would soon become “unmarketable” as the crisis extended into the American railroad bond market.[vii] Cooke needed to sell as many bonds as possible. His brother, Henry, would be the key to his escape; Henry was on the board of the Freedman’s Bank and had an idea for how he may help his brother.[viii] Although the Freedman’s Bank had a reputation for being a governmental institution, it was in fact a chartered savings bank that some 100,000 freed slaves had entrusted with approximately $50 million “between 1865 and 1874.”[ix] Henry, being on the board, secured an amendment to the bank’s charter that changed the bank from a savings bank to an investment bank, and he began to invest the bank’s funds into railroad bonds including some of the worst assets of the Jay Cooke & Company; it did not stop there: the Freedman’s Bank also loaned money to the company and took bonds as collateral that Jay would never have been able to sell on the market.[x] With the market conditions becoming increasingly difficult, one of the most successful railroads of the time had to resort to corrupt dealings to stay afloat, and it would not remain afloat for much longer.

Black Friday came on September 18, 1873 when the New York office for the Jay Cooke & Company closed, and other company offices soon followed.[xi] Panic ensued. The New York Tribune wrote, “Dread seemed to take possession of the multitude.”[xii] Those individuals with deposits immediately sought withdrawal; the New York Stock Exchange shut down “for the first time in its history”; banks began searching for capital by calling on loans (pushing the businesses with those loans to the brink); and the federal government’s response—after bankers pleaded with President Ulysses S. Grant to take action—was limited to the United States Treasury buying up some bonds and reissuing cash to boost inflation.[xiii] The Nation reported: “Great crowds of men rushed to and fro trying to get rid of their property, almost begging people to take it from them at any price.”[xiv] After the panic came an economic depression: by 1876, “roughly half of the railroad companies had gone into receivership” with those receiverships controlling “half the railroad milage” in the country; from 1873 to 1878, railroad stocks lost nearly two-thirds their value; and during the first eighteen months of the depression, half of American iron foundries closed.[xv]

Although more detailed statistics about the depression are not available, it was devastating in scale. Historians have estimated that the economy contracted during the depression for as long as 65 consecutive months.[xvi] Annual bankruptcies grew from 5,183 in 1873 to 10,478 in 1878, the “last full year of the depression,” and those bankruptcies were not limited to railroads: they consisted of “manufacturers, merchant houses, commodity traders, law and accounting offices.”[xvii] Unemployment, a concept that a generation prior—one that did not have pervasive wage labor—would have been mystifying, was estimated to be as high as twenty-five percent in New York City; and with high unemployment came desperation: it was not unheard of for families to resort to eating their pets during this time.[xviii] Then, the unemployed faced a society that shamed them: those who came of age before the wage labor system assumed the unemployed to be disabled or simply lazy, and historians have attributed the widespread unemployment during the depression to “homelessness, malnutrition, crime, and illness.”[xix] Unemployment was not the only new term added to the American lexicon. Those who were homeless became known as “tramps”—a label that (along with “bums”) was common in the Civil War camps—and a subtype of tramps were the “seasonal laborers integral to regional economies,” which became known as “hoboes.”[xx] Regardless of title, those in the lower rungs of work struggled; by the end of the depression, “unskilled workers were worse off than they had been twenty years earlier.”[xxi] The panic, and the depression that followed, would not be the first, last, or largest of its kind. The economy would rapidly recover and continue growing (largely as a result of an influx of immigrants into the United States during the remainder of the Nineteenth Century), but workers could now see the consequences of an expanded market—a market that consisted of wage labor, speculative investments, and ruthless operation.

[i] See Richard White, The Republic for Which It Stands: The United States During Reconstruction and The Gilded Age, 1865-1896, 260.

[ii] See id. at 261.

[iii] See id.

[iv] Id.

[v] Id. at 262.

[vi] Id.

[vii] Id.

[viii] Id. at 265-66.

[ix] Id. at 265.

[x] Id. at 266.

[xi] See id.

[xii] H.W. Brands, American Colossus, The Triumph of Capitalism, 1865-1900, 88.

[xiii] Richard White, The Republic for Which It Stands: The United States During Reconstruction and The Gilded Age, 1865-1896, 266; H.W. Brands, American Colossus, The Triumph of Capitalism, 1865-1900, 89.

[xiv] H.W. Brands, American Colossus, The Triumph of Capitalism, 1865-1900, 88-89.

[xv] Richard White, The Republic for Which It Stands: The United States During Reconstruction and The Gilded Age, 1865-1896, 266-67.

[xvi] Id. at 268.

[xvii] Id.; H.W. Brands, American Colossus, The Triumph of Capitalism, 1865-1900, 89.

[xviii] See Richard White, The Republic for Which It Stands: The United States During Reconstruction and The Gilded Age, 1865-1896, 268.

[xix] Id. at 269.

[xx] Id. at 271.

[xxi] Id. at 272.

Leave a comment